Disclaimer: This post may contain affiliate links. This is one way that bloggers make money, but it is at absolutely no extra cost to you if you choose to make a purchase based on my suggestions! If you would like to read more about how this works, check out my Disclosure Policy!

My Story!

My Story!

If you have been following my story at all, you probably know my story. If not, I tell my story at the beginning of every monthly report for those who just stumbled upon my blog. I gain different followers every month and I don’t want anyone to feel blind as they find my posts! If you have read my story, feel free to skip ahead to my monthly report. I tell this story so I am not just some stranger, but instead someone who just might inspire each and every reader to follow the same journey!

My name is Elyse. I am 23, single with no kids and I am proudly on my way to being completely debt freeeee. I never really thought of myself as someone who was in debt. With no credit cards and no car payment, I was not the average American. All I had was a few student loans. But, it wasn’t until a few weeks before my 22nd birthday that I got a loan for a Jeep and my very first credit card. I should say credit card(s). There were two or three that showed up that month.

For that month of December, I thought it was so cool that I finally had a credit card. I was excited over it actually. I was learning about all the different rewards I could cash in and it was fantastic. Even though I had never needed a credit card, I was determined that I needed them then. I even went on vacation using mostly my credit card. I had racked up a pretty decent amount of money on my credit cards and started picking up extra waitressing shifts to get it cleared. While I have never paid interest on my credit cards, I have definitely gotten close.

Towards the end of the month, I was cleaning off a bookshelf, getting ready to move (again), and found The Total Money Makeover: Classic Edition: A Proven Plan for Financial Fitness. This $15 book completely changed my life path at the time. Dave describes being debt free as such a rewarding and achievable thing. In his book, he says it will take work and it will be hard, but it will be worth it. He has been right. I call this my “God wink” moment because what I needed came into my life as soon as I needed it.

There have been days were I have completely questioned my sanity. I sometimes wonder why I don’t just make minimum payments forever like everyone else. But I also know that someday, I will be able to travel and just stop to enjoy life because I won’t owe any money towards my house, car, college, or credit cards. Knowing that “This too shall pass” has been the motivation to keep me going this year.

“Sometimes, you have to live like NO ONE else, so someday you can LIVE like no one else.” – Dave Ramsey

If you haven’t read the book, I recommend you go buy it RIGHT NOW. It will be $15 that changes your life completely. I will wait, just be sure to come back to read the rest of the post.

I officially started my debt free journey on January 1st, 2017. Originally, my goal was to pay off my debt in one year. Turns out, I don’t actually even make enough money for that to even be a possibility. Read about how I paid off $15,000 on my $38,000 (pre-tax) income last year. My goal is to be debt free by October 2018. I don’t really know how it is going to happen, but the how isn’t important right now! My overall goal is to get completely debt free, buy a house, and continue to save for an even better house! I am extremely excited about the opportunities to come with my journey ahead.

Even if I didn’t make my original goal, Debt Free At 23 has such a great ring to it. Debt free at 24 still isn’t terrible either.

During 2017, I wrote a monthly update every month. During 2018, I lost sight of the monthly updates. But here is my mid-year review of how 2018 is helping me kill my goals.

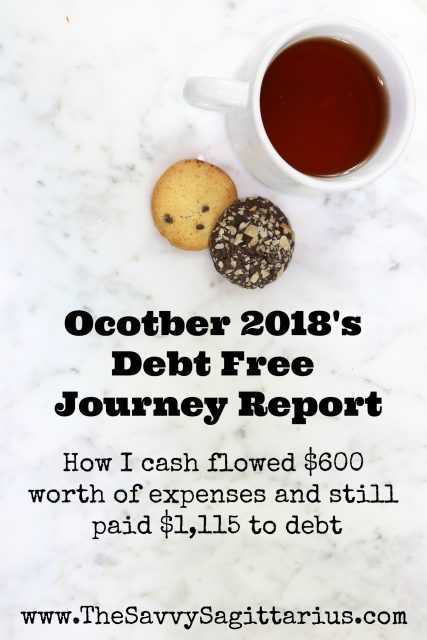

In October 2018, I paid off $1,115 on my last student loan account!

I started in 2017 with 8 accounts and $34,000, but here is what my debt snowball looks like now:

| Debts | Starting Debt | Principle Paid To Date | Debt Left |

| Amazon Card | $ 10.99 | $ 10.99 | PAID JAN 17 |

| Mary Kay Card | $ 275.00 | $ 275.00 | PAID JAN 17 |

| Credit Card | $ 649.88 | $ 649.88 | PAID JAN 17 |

| Student #1 | $ 2,087.41 | $ 2,087.41 | PAID APRIL 17 |

| Jeep | $ 2,500.00 | $ 2,500.00 | PAID JULY 17 |

| Student #2 | $ 3,550.00 | $ 3,550.00 | PAID SEPT 17 |

| Student #3 | $ 4,950.00 | $ 4,950.00 | CONSOLIDATED |

| Student #4 | $ 450.00 | $ 450.00 | CONSOLIDATED |

| Refinanced Student Loan | $ 19,529.00 | $ 13,244.00 | $ 6,285 |

I have less than $6,500 remaining in debt!

Reflection of October 2018:

October was an extremely eventful month. During October 2018, I had to cash flow quite a few expenses.

- New Car Battery: $125

- Year of Amazon Prime: $125

- Energy Supplements: $101

- Fall Festivities (pumpkin patch): About $70

- Moving: About $75 including all of the meals at restaurants because stuff was packed

- Getting my hair done (once a year treat): $112

That is over $600 in cash flowed expenses. While I did use my credit card for expenses throughout the month (like always), I paid everything off on the last day of the month. I do currently still use my credit cards to be able to track my spending because I have found that with cash, I just keep adding cash to the envelopes when I am out.

Looking Forward to November 2018:

Moving will be a huge help on my financial goals because I am about 20 minutes closer to work which will help with my gas savings this month! I am working a few extra shifts throughout the month because of the holidays. Moving also lowered my overall expenses by about $150. After I get some of the final bills take care of from the old apartment, I will be clear to make HUGE debt payments this month.

Two things that I am cash flowing right now are new tires for my vehicle before the winter really hits and Christmas shopping. I just started saving for Christmas because I knew that I would just spend the money if I started earlier in the year. I am trying to spend less on the holidays this year. This means that the less money that I save for the holidays, the less I have to spend on the holidays. My plan is to cash out my credit card rewards from the year, and plan carefully! Check out my other tips for saving money on Christmas this year!

Things that helped me in October 2018:

Setting Realistic monthly goals

I have been using my server budget system!

These 8 Financial apps that I am still using!